So what Medicare Supplement plan do I

choose?

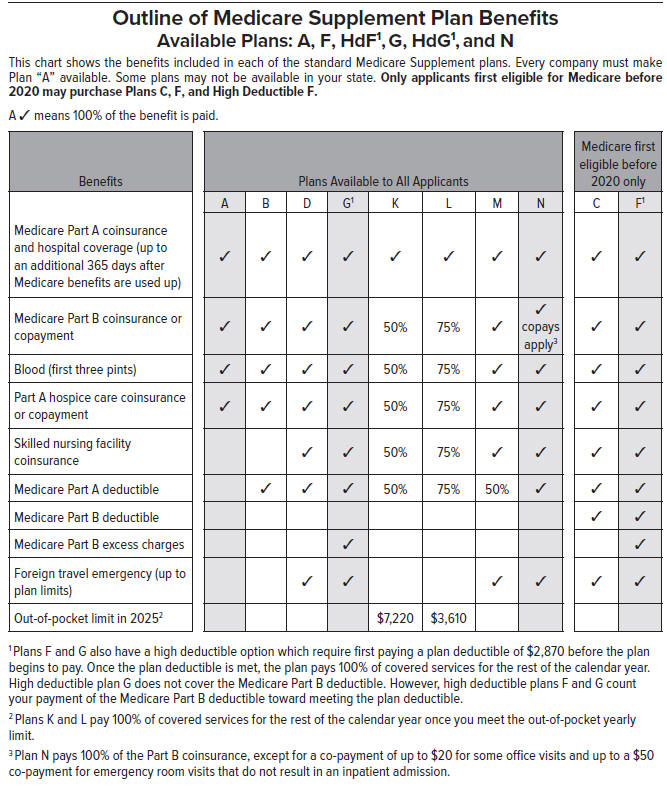

Medicare Supplement Policies

Medicare Supplement

Insurance plans, also known as Medigap, are designed to help cover

the out-of-pocket costs that Original Medicare (Parts A and B)

doesn't cover, such as copayments, coinsurance, and deductibles.

These plans are standardized by the federal government, meaning that

the benefits of each plan letter are the same across different

insurance companies, although the premiums can vary. It's important

to note that Medigap plans generally don't include prescription drug

coverage, so a separate Medicare Part D plan is needed for that.

Also, those newly eligible for Medicare on or after January 1, 2020,

cannot purchase Plan C or Plan F.

Ranking Medicare

Supplement policies from best to most basic coverage can be complex,

as the "best" plan depends on an individual's healthcare needs, risk

tolerance, and budget. However, we can generally categorize them

based on the comprehensiveness of their coverage.

Here is a general

overview of the 10 standardized Medicare Supplement policies,

keeping in mind that Plans C and F are only available to those who

were eligible for Medicare before January 1, 2020:

1.

Plan F (For

those eligible for Medicare before 2020):

●

Coverage: This plan typically offers the most

comprehensive coverage, often covering the Part A deductible, Part B

deductible, Part B coinsurance, Part A coinsurance, skilled nursing

facility care coinsurance, hospice care coinsurance or copayment,

and blood (first 3 pints). Some Plan F policies also offer coverage

for Part B excess charges.

●

Why it's often considered top: It leaves

beneficiaries with the least out-of-pocket expenses for

Medicare-covered services.

2.

Plan G:

●

Coverage: Plan G covers almost everything that

Plan F covers, except it does not pay the annual Medicare Part B

deductible.

●

Why it's highly rated: For those newly eligible

for Medicare, Plan G offers the most comprehensive coverage

available and often has lower premiums than Plan F, potentially

leading to overall savings.

3.

Plan C (For those eligible for Medicare before 2020):

●

Coverage: Plan C covers the Part A deductible,

Part B coinsurance, skilled nursing facility care coinsurance,

hospice care coinsurance or copayment, blood (first 3 pints), and in

some cases, foreign travel emergency care.

●

Key difference from F: Plan C does not cover

Part B excess charges.

4.

Plan N:

●

Coverage: Plan N covers the Part A deductible,

Part B coinsurance (except for copays of up to $20 for some office

visits and up to $50 for emergency room visits that don't result in

inpatient admission), skilled nursing facility care coinsurance,

hospice care coinsurance or copayment, and blood (first 3 pints).

Some policies may also cover foreign travel emergency care.

●

Why it's popular: Plan N often has lower

monthly premiums compared to Plans F and G, making it an attractive

option for those comfortable with small copays.

5.

Plan D:

●

Coverage: Plan D covers the Part A deductible,

Part B coinsurance, skilled nursing facility care coinsurance,

hospice care coinsurance or copayment, and blood (first 3 pints).

Some policies may also cover foreign travel emergency care.

●

Key difference from G: Plan D does not cover

Part B excess charges.

6.

Plan M:

●

Coverage: Plan M covers 50% of the Part A

deductible, Part B coinsurance, skilled nursing facility care

coinsurance, hospice care coinsurance or copayment, and blood (first

3 pints). It may also cover foreign travel emergency care.

●

Key feature: Plan M includes an out-of-pocket

limit.

7.

Plan K:

●

Coverage: Plan K covers 50% of the Part A

deductible, 50% of Part B coinsurance, 50% of skilled nursing

facility care coinsurance, 50% of hospice care coinsurance or

copayment, and 100% of blood (first 3 pints) after you meet the Part

B deductible.

●

Key feature: Plan K has an annual out-of-pocket

limit.

8.

Plan L:

●

Coverage: Plan L covers 75% of the Part A

deductible, 75% of Part B coinsurance, 75% of skilled nursing

facility care coinsurance, 75% of hospice care coinsurance or

copayment, and 100% of blood (first 3 pints) after you meet the Part

B deductible.

●

Key feature: Plan L has a higher annual

out-of-pocket limit than Plan K.

9.

Plan B:

●

Coverage: Plan B covers the Part A coinsurance

and hospital costs up to an additional 365 days after Medicare

benefits are used, Part B coinsurance, blood (first 3 pints), and

Part A hospice care coinsurance or copayment. It also covers the

Part A deductible.

●

What it lacks: It does not cover the Part B

deductible, skilled nursing facility care coinsurance, or Part B

excess charges.

10.

Plan A:

●

Coverage: Plan A offers the most basic

coverage, including Part A coinsurance and hospital costs up to an

additional 365 days after Medicare benefits are used, Part B

coinsurance, blood (first 3 pints), and Part A hospice care

coinsurance or copayment.

●

What it lacks: It does not cover the Part A

deductible, skilled nursing facility care coinsurance, Part B

deductible, or Part B excess charges.

Ranking from

Most to Least Comprehensive Coverage (General Guide):

1.

Plan F

(For those eligible for Medicare before 2020)

2.

Plan G

3.

Plan C

(For those eligible for Medicare before 2020)

4.

Plan N

5.

Plan D

6.

Plan M

7.

Plan L

8.

Plan K

9.

Plan B

10.

Plan A

Important

Considerations:

●

Availability: Plans C and F are not available

to those who became eligible for Medicare on or after January 1,

2020.

●

Premiums: Generally, plans with more

comprehensive coverage (like F and G) tend to have higher monthly

premiums. Plans with less coverage (like A and B) usually have lower

premiums but result in higher out-of-pocket costs when you need

healthcare services. Plans K and L have lower premiums but require

you to pay a percentage of the costs until you reach your

out-of-pocket limit.

●

High-Deductible Options: Plans F and G may also

be available as high-deductible versions in some states, offering

lower premiums but requiring you to meet a significant deductible

($2,870 in 2025) before the plan starts paying.

●

Individual Needs: The "best" plan truly depends

on your individual health needs, how often you anticipate needing

medical care, and your financial situation. If you prefer

predictable costs and want more comprehensive coverage, a plan like

G might be suitable. If you are relatively healthy and want a lower

premium, Plan N or even a cost-sharing plan like K or L might be

considered.

It's recommended to

carefully compare the benefits and premiums of different Medigap

plans available in your area to make an informed decision that

aligns with your specific circumstances. Consulting with a Medicare

advisor can also be beneficial.

|